Robotics is playing a greater role in the insurance claim market generally and has growing room for expansion within marine insurance more specifically.

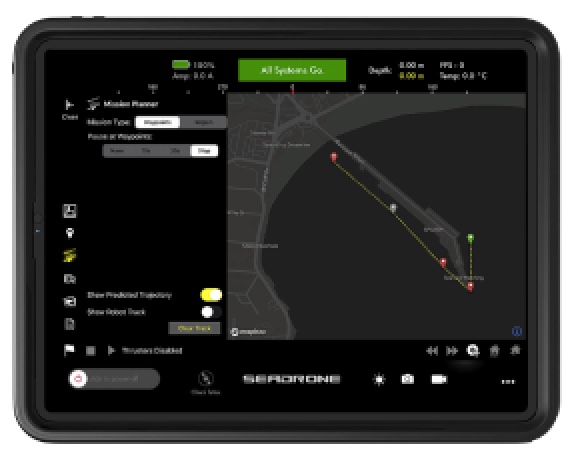

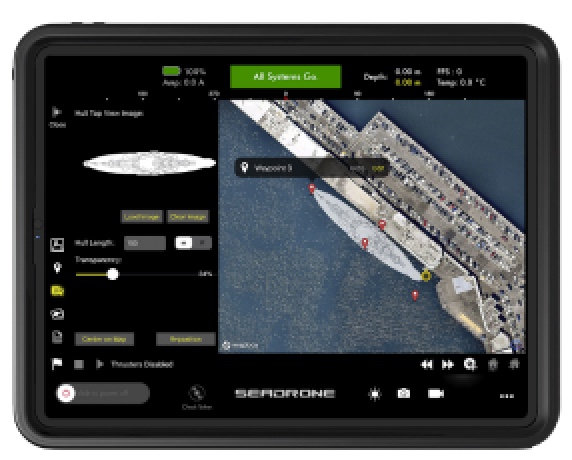

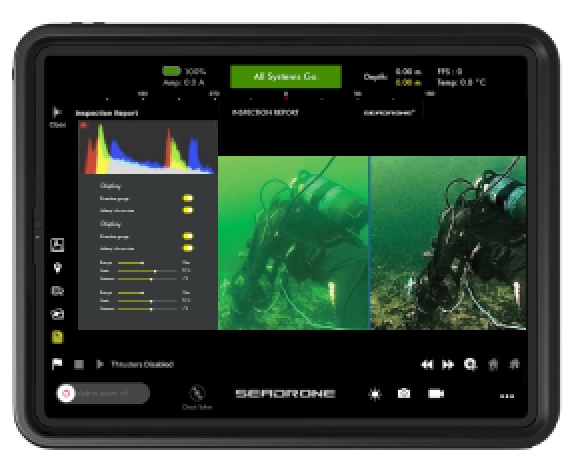

After a storm, collision, or other incident results in damage to a ship, the ship operator will often file an insurance claim. Insurers will then most likely need to verify these claims by sending a marine insurance inspector or surveyor to inspect the ship. This inspection might involve the use of an underwater ROV. However, the surveyor is not usually a trained expert in robotic piloting, or may not have as easy of access to the ship as someone already onsite. That’s why some within the marine industry are turning to Robotics Process Automation (RPA) and video technology powered by Artificial Intelligence (AI). The use of underwater ROVs such as the SeaDronePRO for ship inspections may also prove to be an extremely useful addition to this growing robotics toolkit.

Robotics Process Automation (RPA)

Robotics Process Automation (RPA) has become more standard within the insurance industry. Tokio Marine Kiln (TMK) adopted RPA in the summer of 2018, tapping NTT DATA UK for its robotics services.

Insurance companies are also using visual evidence, particularly video, powered by Artificial Intelligence (AI). In May 2020, Tokio Marine successfully tested an AI-driven solution for auto insurance claim processing in Japan which could in future be expanded to the marine industry.

Types of Marine Insurance Policies

Marine insurance covers the loss or damage of ships, of cargo, and of terminals where cargo is loaded and unloaded. The first two – ships and cargo – are the most common types[CK1] . Marine insurance is often grouped with Aviation and Transit risks, known together by the acronym MAT. Marine insurance claims may cover the following classes of business:

Hull and Machinery (H&M)

Marine cargo

Freight insurance

Liability insurance

Terminals

War risk

Building risk

Rigs

Specie (cash, fine art, or another valuable product)

Certain risks make these coverages necessary, including:

Collisions

Grounding

Fire

Explosion

Natural disasters such as earthquakes or hurricanes

Accidents in moving cargo or fuel

Piracy or terrorism

Examples of recent hulls claims which involved these risks include the 2012 grounding of the Costa Concordia that resulted in a USD 2 billion loss and is still the largest loss in the last decade, loss of the Bulk Jupiter in 2015 and Emerald Star in 2017 likely due to cargo liquefaction (the abrupt transformation of solid materials like iron ore into an almost liquid state), and the fire and sinking of the oil tanker Sanchi off the coast of China in January 2018.

Containership fires have proved to be some of the most ubiquitous risks, due to the shipping of large amounts of flammable or hazardous materials made possible within the widely used intermodal box container developed in 1956.

Despite costly instances, there have been relatively few major losses in recent years. Some of the large hull and cargo losses in recent years have been due to natural catastrophes, particularly storms and hurricanes, though the frequency of major hull claims remains low.

More Types of Marine Insurance

Insurance coverage is most often either on a "voyage" or "time" basis, covering transit between ports or a time period typically of one year. The time basis coverage is the more common of the two. Types of insurance may include:

Time

Voyage

Floating

Construction or Building

A restricted form of coverage is known as "Total Loss Only" (TLO), generally used as a reinsurance, and which only covers the total loss of the vessel and not any partial loss.

Many of the concepts that govern insurance generally also apply to marine insurance, including the seven principles that are covered in all marine insurance contracts:

Utmost Good Faith – the insured (policy holder) and insurer (insurance company) act in good faith toward each other

Insurable Interest – the contract must provide possible financial gain

Proximate Cause – something you are not insured for nearby what you are insured for may cause the damage

Indemnity – a guarantee of compensation

Subrogation – the substitution of one insurance company for another

Contribution – if you are insured by multiple companies, they will

Loss Minimization – it is the responsibility of the insured (policy holder) to do take all preventative action to minimize damage or loss

1906 Marine Insurance Act

A well-known piece of marine insurance history lore is that in the late 1680s, Edward Lloyd opened a London coffee house that became popular amongst the ship owners, merchants, and ship captains of the day, and consequently became a reliable source of information on the latest shipping news. Soon Lloyd’s Coffee House transformed into the first marine insurance market. It became the meeting place for parties in the shipping industry wishing to insure cargoes and ships, and those willing to underwrite such ventures. These informal beginnings led to the establishment of the insurance market Lloyd’s of London and several related shipping and insurance businesses. The participating members of the insurance arrangement eventually formed the Society of Lloyd’s, not to be confused with Lloyd’s Register. Though perhaps not as well documented in its origins, the practice of marine insurance is thousands of years old, perhaps dating back to the Phoenician traders. The most critical movements in marine law began to take place in the latter part of the 18th century.

Marine insurance was first codified in the 1906 Marine Insurance Act by Sir Mackenzie Chalmers, who compiled centuries of judicial precedent and about 2,000 cases into their most relevant principles. The standard policy (known as the “SG form”) was updated in 1991 with wording known as the MAR 91 form. A crucial difference between marine insurance and non-marine insurance is that the insured may not always have to prove his/her loss, most notably in the case of a sunken vessel.

Today, the International Union of Marine Insurance (IUMI) represents national and international marine insurers, lobbying organizations such as the International Maritime Organization (IMO) and other specialist agencies to defend IUMI’s member interests. IUMI also plays a networking and knowledge sharing role, holding its annual conference in September (this year’s was virtual due to COVID-19).

What happens when you file a claim?

When shipping cargo are destroyed, damage or stolen, a marine insurance claim is made to the insurance company. The insurance company will then verify that reasonable care was taken during cargo transport. Simultaneously, the insured must make a claim with the shipping company to notify them of damage. In many places the time window for lodging a claim for marine insurance is about one year from the date of the discharge of the cargo, though this may vary amongst insurers. The insurance company then appoints a surveyor, who visits the cargo loss or damage site and submits a report based on the findings to his/her insurance company.

Protection and Indemnity (P&I) Clubs

P&I Clubs are formed when there is mutual pooling of risk by ship owners, and they cover liabilities of ship owners to cargo owners and third parties.

Marine insurance has a rich history dating back centuries, with legislation both anchored in precedents and evolving according to its time. As the industry moves into a modern era of digitalization, robotics has a greater role to play. Underwater ROVs such as the SeaDrone PRO are a useful part of the growing robotics toolkit. It continues to be a space to watch.

Visit SeaDronePro.com for more information.

“Insurers will then most likely need to verify these claims by sending a marine insurance inspector or surveyor to inspect the ship.”

“The first two – ships and cargo – are the most common types.”

The oil tanker Sanchi in January 2018, after cargo liquefaction caused a fire. This was one of the largest insurance claims filed in the past decade. / IRNA / phys.org / Home - Earth- Environment

“Is that in the late 1680s, Edward Lloyd opened a London coffee house that became popular amongst the ship owners, merchants, and ship captains of the day, and consequently became a reliable source of information on the latest shipping news.”

Lloyd’s of London, the early days (1808) / Spartacus Educational / British Story - London

“Marine insurance was first codified in the 1906 Marine Insurance Act.”